Garren Work, MBA

VP, Mergers & Acquisitions Advisor for Businesses <$100MM

Click here to view original article

The M&A landscape often sees disruption during election years, driven by potential changes in regulation, economic conditions, and tax policies. The 2024 election cycle is no different, bringing these uncertainties to the forefront. Strategic opportunists with a long-term focus should continue their search efforts but could become more selective. Meanwhile, contemplative Sellers often take a “wait and see” approach, remaining optimistic. However, failing to prepare for policy changes can be costly, as late reactions can hamper an exit plan if the business isn’t prepared for coming changes.

Election Overview

The 2024 contest appears set (for now). Donald Trump has officially [i] became the Republican nominee, selecting JD Vance as his running mate. The Democratic nominee, made official in August, is Vice President Kamala Harris following incumbent Joe Biden’s announcement to drop out [ii].

At the time of this writing, FiveThirtyEight’s forecast is currently suspended [iii]. However, prior to Biden dropping out, it predicted an even 50/50 chance between the two candidates, with most media reporting better odds [iv] for Democrats following Harris’s rise.

Regulation Proposals Impacting a Business Sale

From tariffs to OSHA rules, the candidates have several regulation proposals that can impact business, many of which are industry-specific and others widely impacting. Business owners should be aware and prepared for any regulations on the ballot. Here is an example with a deep dive from each candidate:

Trump:

- Major Agenda Item: Removing [v] regulation mandating auto manufacturers produce 67% of new vehicles to be fully electric.

- M&A Impact: This dramatic reversal likely causes all dealmakers in the auto industry to take a “wait and see” approach, halting M&A activity until election day.

- Businesses Impact: This policy change affects not only the auto manufacturers, but also their OEMs, secondary suppliers, and even service providers, which are often overlooked.

Harris:

- Major Agenda Item: Following the DNC agenda, she’s expected to push [vi] for raising the federal minimum wage to at least $15/hour.

- M&A Impact: Buyers analyzing financials may adjust labor costs in anticipation of this, pricing in this raise, reducing expected cashflow, and lowering valuations.

- Businesses Impacted: This would broadly impact lower-margin, labor intensive businesses, like retail, restaurants, and healthcare. The change would be especially impactful in States without minimum wages above the federal minimum – possibly doubling their cost of labor.

Taking a company to market that is ill-prepared for any coming regulations will almost certainly warrant a discount on valuation. Discounts can be mitigated through deal structure, but typically at the cost of buyer-favorable terms on seller financing, including earnouts, or even indemnifications.

Economic Conditions to Watch

Current economic conditions are influenced by:

- Inflation – While decreasing, June’s [vii] inflation was 3%, still above the 2% target. This remains a challenge for all businesses, requiring attention to financial metrics. It continues to complicate historical financial comparisons, putting pressure on Buyers to get a firm understanding on performance.

- Low Unemployment – Currently at 4.1% [viii], within the consensus ideal range of 3%-5%, implying an economy at full capacity. Within this range, owners who are not willing to invest in long-time quality and highly paid workers often struggle to fill open roles, adding risk of falling behind. On the other hand, it leads Buyers towards optimistic performance expectations.

- High interest rates – The Prime rate remains steady at 8.5%, a 20-year high. Higher interest rates impact M&A, driving down values as lending costs increase. Current expectations [ix] are the first .25% rate cut in September, but the goal post moves each week.

Both campaigns continue to make bold promises to reduce inflation and interest rates while maintaining employment. Controlling the economy for a “soft landing” might [x] actually be possible and remains the goal with the idea that sluggishness is better than recession.

Assuming Harris remains supportive of Biden’s FY 2025 budget, though yet to pass, trouble may be ahead. An analysis by the Tax Foundation estimates [xi] the budget will reduce GDP by -1.6% in the long run and may lead to further inflation.

Meanwhile, some analysts claim the stock market is currently pricing in[xii] a Trump victory, with all major indices near all-time highs. Since public markets have a major influence in valuations at all levels, Sellers should get excited but reserve caution that the public markets can be reactive and are pricing in a 70%+ chance of a Trump victory, which greatly differs from most pollsters.

Economic outlook often impacts an individual’s decision on timing to acquire or sell. Many may choose to “wait and see” hoping for stability or “greener grass” ahead. Unfortunately, timing the market carries risk along with possible reward, with experts estimating over 50% chance [xiii] at a recession over the next 12 months.

Failing to develop an exit plan can leave owners over-exposed to impacts from any recession. A business sale can easily take 6-12 months, remaining exposed to risk from recession which can impede the deal process. Any performance decline during this process creates major challenges to reach the finish line on a deal. Mistiming and a compulsory need to sell may lead to a fire sale, a very difficult outcome to accept.

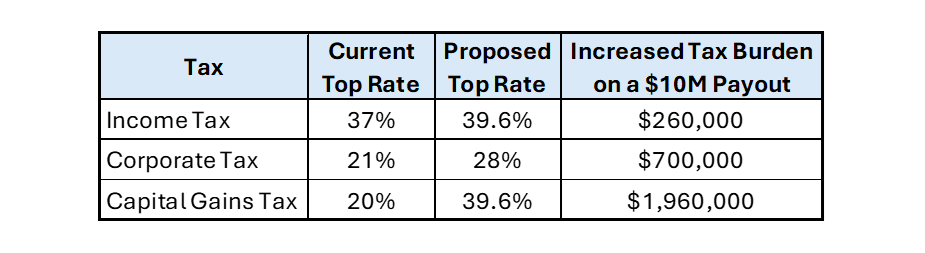

Tax Policy Changes Impact on Proceeds and Value

Tax policies this election cycle arguably have the most direct impact on M&A, especially for Sellers in the in the Lower Middle Market. This is where the candidates’ platforms are also the most polarized.

- Trump: Trump’s 2017 Tax Cuts and Jobs Act fell short of making permanent changes, with those tax cuts set to expire in 2025, during the next administration. He is campaigning [xiv] on making those tax cuts permanent and promises to “pursue additional tax cuts” without much detail.

- Harris: Harris is expected to let those tax-cuts expire, effectively increasing income and corporate taxes. Additionally, the White House is proposing [xv] sweeping tax hikes to the capital gains tax and promises to eliminate “like-kind exchange loopholes”, commonly known as the 1031 exchange. While 1031 exchanges don’t typically apply directly to business sales, they can apply to any real estate which, if owned, is often transacted simultaneously along with the business.

These proposed tax differences can impact Buyer’s post-tax earnings expectations, making acquisitions less attractive since Buyers typically consider post-tax ROI. For Sellers, these proposals can make a big difference in the tax burden on the Seller’s proceeds from a transaction, typically earmarked for retirement funds. In the LMM, these proceeds are typically considered goodwill, which is taxed as capital gains.

Below is an example that demonstrates how an increase in the respective tax rate would directly impact a Seller’s “take-home” payout:

For instance, a goodwill sale with $10 million in pre-tax proceeds would cost the Sellers an additional $2M in taxes. This variance disrupts any existing exit strategies, requiring Owners to revisit their exit/retirement plan if these proposals are passed. Dealmakers may be able to develop creative deal structures mitigating some of this cost but would require a Seller to spread out the payments over multiple tax years, which is typically less appealing to Sellers.

Conclusion

The 2024 election cycle brings complexities, impactful tax concerns, and overall uncertainty causing many dealmakers to adopt a “wait and see” approach to M&A strategies. However, business owners can take action to navigate these challenges effectively and mitigate risk.

First, Business Owners should stay ahead of regulatory changes, staying aware of how various policy proposals impact your industry. Buyers may find opportunities where Sellers failed to prepare for coming changes and add value through implementing required changes.

Second, engaged Owners who actively monitor their business’s financial metrics through current challenges have a better chance to defend any pressures from macroeconomic factors such as inflation or even a recession. When market conditions improve, these businesses should be in a better position to grow or attract Top Dollar offers. Additionally, Owners who better understand how performance and market conditions impact their company’s valuations will be better positioned to time the market or possibly find value focused add-on opportunities.

Third, soon-to-be Sellers should understand the impact of tax proposals on their take home proceeds, especially if relying on these funds as their retirement fund. Should the election swing in favor of Harris and she implements the current tax proposals, there may be a short strategic window to pursue a sale and avoid excessive tax burdens. While current market conditions are not ideal, there is merit for Sellers to explore now, locking in value after surviving a tumultuous post-covid era with a known tax burden, especially if market conditions don’t improve post-election.

Last, be sure to cast an informed vote in November!

[i] https://www.cbsnews.com/news/rnc-roll-call-of-states-2024/

[ii] https://www.cnn.com/2024/07/21/politics/video/biden-drops-out-of-presidential-race-digvid

[iii] https://projects.fivethirtyeight.com/2024-election-forecast/?cid=rrpromo

[iv] https://www.pbs.org/newshour/politics/where-harris-and-trump-stand-after-biden-leaves-the-race

[v] https://www.donaldjtrump.com/agenda47/president-trumps-message-to-americas-auto-workers

[vi] https://democrats.org/where-we-stand/party-platform/building-a-stronger-fairer-economy/

[vii] https://tradingeconomics.com/united-states/inflation-cpi

[ix] https://abcnews.go.com/Business/fed-expected-cut-interest-rates-week/story?id=112364515

[xi] https://taxfoundation.org/research/all/federal/biden-budget-2025-tax-proposals/

[xii] https://www.reuters.com/markets/global-markets-wrapup-1-2024-07-14/

[xiv] https://www.cnn.com/2024/04/10/politics/trump-2017-tax-cuts-rich/index.html